In the spring of 2019, Cory Dowd suddenly found himself without health insurance for the first time. A self-employed event planner, he had just finished a Peace Corps stint that provided health benefits, but he was still more than a year away from starting a graduate program that would provide coverage through his university.

So, like countless others in an online world, he went insurance shopping on the internet.

But the individual insurance market he was about to enter was one dramatically changed under President Donald Trump’s push to dismantle Obamacare, offering more choices at cheaper prices.

Dowd is well-educated and knew more than most about how traditional health insurance works. But even he did not understand the extent to which insurers could offer plans that looked like a great deal but were stuffed with fine print that allowed companies to deny payment for routine medical events.

Not bound by the strict coverage rules of the Affordable Care Act, the short-term plans that Dowd signed up for have been dubbed “junk insurance” by consumer advocates and health policy experts. The plans can deny coverage for people with preexisting conditions, exclude payments for common treatments and impose limits on how much is paid for care.

Dowd, like millions of other Americans who have flocked to such plans in the past three years, only saw what looked like a great deal: six-month coverage offered through an agency called Pivot Health, whose website touts the company as a “fast-growing team obsessed with helping you find the right insurance for your needs.”

Monthly premiums for the two short-term plans he bought were surprisingly cheap at around $100 a month each, with reasonable co-pays for routine doctor visits and treatments. Best of all, the first plan he bought promised to cover up to $1 million in claims, the second up to $750,000. That should more than do it, he thought. Dowd was 31 and healthy but wanted protection in case of a medical emergency. He signed up and began paying his premiums without closely reading the details.

Then he was hit with the very kind of emergency he had feared. And he wasn’t protected after all.

Short-term plans have been around for decades, and are meant to temporarily bridge coverage gaps. Under the Obama administration they were limited to three months. But when the Trump administration allowed them to be extended to nearly a year, they became a fast-growing and lucrative slice of the insurance industry.

Because these plans are not legally bound by the strict rules of the ACA, not only do they come with hefty restrictions and coverage limitations, but insurers can search through patients’ past medical histories to find preexisting conditions.

All companies selling short-term plans have to do is acknowledge that they are not ACA-compliant and may not cover everything — a disclosure the insurers insist they do.

Still, the Biden administration faces a challenge on what to do about the proliferation of such plans.

Once in office, President Joe Biden quickly moved to make enrolling in comprehensive ACA coverage easier and make plans more affordable. On Thursday, the Department of Health and Human Services announced 940,000 people had signed up for ACA plans this spring after enrollment was reopened in February. In many states, enrollment will run through the summer.

Yet, while health policy experts say ACA expansion is important, it does not specifically address those who remain in plans outside the health care law and could be at risk for financial ruin.

“The Biden administration is going to have to find a way to put the genie back in the bottle,” said Stacey Pogue, a health policy analyst for Every Texan, an Austin-based advocacy group.

True numbers of how many people have noncompliant plans remain elusive, as such plans often fly under regulatory radar and industry tracking. Still, an investigation last year by the U.S. House Committee on Energy and Commerce concluded that at least 3 million consumers had short-term limited duration plans in 2019, the last year for which information was available. That was a 27% jump from the previous year, when deregulation began in earnest, the investigation found.

“I would not be surprised if the numbers increased even more last year,” said committee chair Frank Pallone Jr., D-N.J., in an emailed statement. He and others worry that people who lost employer-sponsored health coverage during the pandemic may have been drawn to short-term and other noncompliant insurance without fully understanding what they were buying.

Short-term insurers also do not have to adhere to the ACA rule on how much money they can take for overhead and profit — which means they can pay out less in claims.

Under the health care law, insurers are generally allowed to keep only about 15 to 20 cents of every premium dollar collected, or else be forced to offer rebates to customers. The rule was created to ensure most of the money collected under the ACA went to member claims and quality improvement.

But a ProPublica analysis of 2020 insurance company financial filings found that insurers offering plans outside the law typically kept higher percentages of premiums collected, sometimes much higher.

For instance, Golden Rule, a United Healthcare subsidiary and the nation’s largest issuer of short-term plans, collected $1.6 billion in premiums in 2020 from its various offerings, up from $1.47 billion the previous year. Of that, the company paid roughly 58% toward members’ medical claims in 2020, according to year-end financial statements submitted to the National Association of Insurance Commissioners, a regulatory organization. In 2019, about 62% went to claims, the filing showed.

Companion Life Insurance Company, a subsidiary of BlueCross BlueShield of South Carolina that underwrites plans sold by Pivot Health, including the one Dowd bought, paid out about 67% in health and accident claims from the $294 million in premiums it collected last year, according to its filing.

One notable filing was that of Florida-based American Financial Security Life Insurance Company, which underwrites short-term and other noncompliant plans. Last year, according to its filings, AFSLIC paid just 26% in health and accident claims out of the $31 million it collected in premiums. It is nearly the exact opposite of what the ACA demands of insurers.

“That is simply outrageous. No other word for it,” said Ken Janda, former CEO of a Houston-based regional insurance company who is now an adjunct professor in population health at the University of Houston College of Medicine and who reviewed the financial filings for ProPublica. “It’s a breach of trust.”

Mike Camilleri, CEO of AFSLIC, dismissed the criticism and said it is misleading to base his company’s loss ratio on its premiums collected versus claims paid. He said those reported numbers do not reflect the full financial picture by taking into account financial reserves or claims submitted but not yet paid. A truer percentage would be “in the mid-50s,” he told ProPublica.

Companies offering noncompliant plans also say it is inaccurate and unfair to compare their plans to those offered under the ACA. Because the narrower plans are typically cheaper, insurers say, they need to take a higher percentage of consumer premiums to cover administrative costs per policy.

“Short term insurance provides an important and affordable option for many consumers in need of temporary and flexible coverage lengths,” Maria Gordon Shydlo, a UnitedHealthcare spokesperson, said in an emailed statement regarding Golden Rule.

While short-term plans are not for everyone, she said, limiting access to them “may have unintended consequences in increasing the number of uninsured.”

BlueCross BlueShield of South Carolina did not respond to multiple email and phone requests for comment.

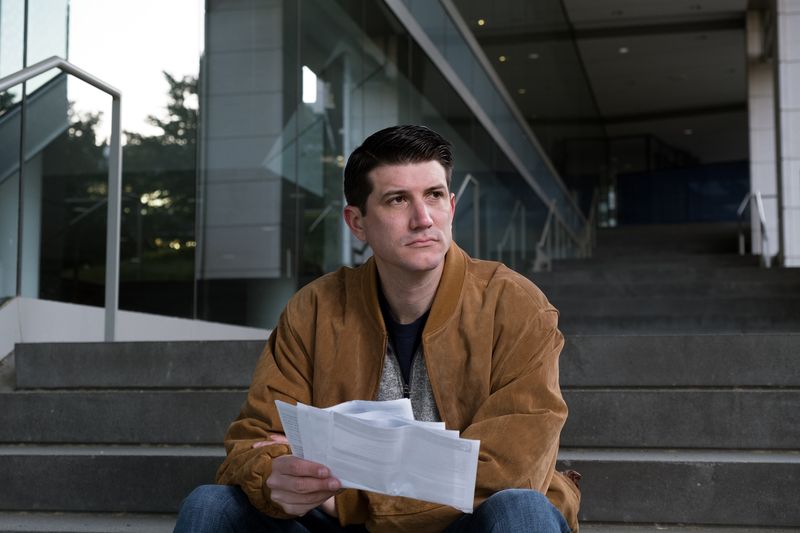

Last July, Cory Dowd’s nagging abdominal pain was getting worse. At the emergency room at Mather Hospital in Port Jefferson, New York, near where he was temporarily living with his mother during the pandemic, he was diagnosed with appendicitis and had a routine appendectomy.

He assumed his insurance would cover the cost. Then he started getting notices of overdue medical bills. The initial hospital bill totaled more than $41,000.

By November 2020, a final hospital statement showed insurance had paid just $1,682 and Dowd still owed $33,600. By then, he was at Duke University pursuing graduate degrees in business and public policy and had no idea what to do.

When the hospital’s billing office urged Dowd to file an insurance appeal, he dug into his policy paperwork. As he read through a long list of exclusions and disclaimers, he found one addressing surgical services that limited coverage to “usual and customary charges, not to exceed $2,500 per surgery.”

“I do have to wonder exactly what kind of surgical procedure can be had for $2,500," he said in a mix of fury and frustration.

When told of Dowd’s experience, Jeff Smedsrud, Pivot’s CEO, said he was surprised and advised Dowd to appeal directly to Pivot. He criticized the hospital for billing Dowd what insurance did not pay.

“They should accept the amount,” he said of the $1,682 insurance payment.

Mather countered that the insurer is at fault for not living up to its contract with the hospital to pay 85 percent of charges. The hospital appealed the insurance payment but lost, a hospital spokesperson said in an email.

The hospital spokesperson added that the insurer had told the hospital Dowd was responsible for any balance because his short-term plan did not fully cover the treatment. Dowd recently applied to the hospital’s financial assistance program, which put a hold on further bills while his case is considered.

On Friday, Dowd told ProPublica he received an email the day before saying his insurer would pay all but $836 of the hospital charge. On Monday, a Mather spokesperson confirmed a check for $32,772 had been received and that the remaining balance would be waived by the hospital.

The whole thing has left Dowd reeling.

“It’s one thing for a company to create a cheap plan designed to cover some basic expenses,” he said. “It’s another to market these plans with maximum benefits as high as $750,000. I am hard-pressed to imagine them ever getting close to those maximums with restrictions like $2,500 for a surgery. It seems these insurance policies are not created and sold in good faith but are designed to look like legitimate plans that don’t cover what the policy holders expect."

In late 2017, the Republican-led Congress slipped into its sweeping tax reform bill a provision to eliminate the penalty for failing to have health insurance that meets the ACA’s criteria. While the individual mandate remained — a cornerstone of the law requiring most everyone to have comprehensive coverage — the deterrent for violating it disappeared.

Then, just weeks later, the Trump administration proposed a new rule to extend short-term plans to just shy of one year, with the option to renew for up to three years. The new rule also allowed short-term insurers to retain medical underwriting, an industry practice of basing coverage and price on the insured’s medical history. It is illegal in ACA-compliant plans.

The short-term plan expansion was quickly challenged by critics but went into effect in the fall of 2018; it was upheld by a federal judge the year after and an appeals court panel last year. Some individual states, however, have since acted to limit the plans’ duration and scope.

The Trump White House vigorously defended its deregulatory actions as friendly to both consumers and taxpayers. Eliminating the penalty for having a non-ACA-compliant plan “will enable consumers to decide for themselves what value they attach to purchasing insurance,” according to a 2019 White House Council of Economic Advisers report on deregulation.

The report did, however, acknowledge pitfalls: “Some consumers who choose not to have ACA-compliant coverage might have higher healthcare expenditures than they expected and lack coverage. This would not necessarily mean these consumers were unwise in their choice of insurance; they were unfortunate.”

“This isn’t a coincidence,” said Dania Palanker, assistant research professor at the Center on Health Insurance Reforms at Georgetown University. “The administration loudly signaled that short-term plans should be sold as cheap long-term coverage. The telemarketers and lead generating websites heard the signal loud and clear.”

Complaints to consumer advocacy groups and state regulatory offices began to surface of vague if not outright fraudulent coverage promises, including assurances that the narrower plans were as good as or better than individual plans offered on the ACA exchange.

Shopping online has proven especially tricky. Paid advertisements often appear atop searches for health insurance, with names that imply ACA compliance, such as obamacare-plan.com or HealthCare.com.

The 2020 congressional investigation found that broker enrollment for short-term plans rose 120% toward the end of 2019 ACA open enrollment, which suggests the marketers were especially aggressive as people searched for coverage.

Pushing the plans was also lucrative, the investigation found. Brokers selling noncompliant plans earned on average a 23% commission on every plan sold. The average commission rate for an ACA-compliant plan was 2%.

In March 2020, just as the pandemic took hold, Brookings Institution researchers launched a “secret shopper” experiment to gauge how those selling noncompliant plans answered questions about COVID-19 coverage.

Posing as an uninsured 36-year-old single woman with no preexisting conditions, senior research assistant Kathleen Hannick called nine brokers or agents in three states to ask about short-term plans. Hannick declined to name the companies or the states.

When asked if the plans covered COVID-19 treatment, the salespeople were quick to offer reassurance, she said. But once the pitches were checked against plan documents, the majority of the answers were false, unclear or misleading. Similarly, five of six salespeople gave inaccurate or misleading answers about when COVID-19 would be considered a preexisting condition that could limit future coverage.

“Not until a doctor says you got it,” Hannick said one broker replied. “You can have symptoms all day long; you don’t know what that is. That could be the flu.” The broker encouraged getting a policy “now, before that happens.”

Such advice contradicts plan terms defining a preexisting condition and also fails to disclose possible scrutiny of past medical conditions or coverage waiting periods.

“Going into the calls I was not prepared for receiving information that was just false,” Hannick told ProPublica. “It’s startling to think how many people might have gone into the pandemic with a false sense of security regarding how much coverage they actually had.”

Katrina Black, who graduated from Harvard Law School in 2019, began looking for health insurance that summer. Then 26, she had just moved from Boston to Austin, Texas, after undergoing endometriosis surgery in Massachusetts while covered under a student plan.

Her new job as a nonprofit lawyer provided health benefits but didn’t start until fall, and she needed coverage immediately to continue post-surgical treatment. She typed “healthcare.gov” into her computer, hoping to find an ACA plan with a subsidy to lower the cost. A pop-up appeared asking for her zip code and phone number. She entered both, not knowing she was being steered away from the government site.

Within minutes, her phone began ringing. It rang continuously for days as brokers tried to sell her health plans, many of which she had never heard of before.

One broker even apologized for the telemarketing bombardment. “What do you need?” she recalled the broker asking.

Black explained she wanted a thorough, affordable plan to briefly cover costs of ongoing care, including several physical therapy sessions a week, medical tests and specialist appointments.

When told that she would be covered, Black said she and her husband enrolled with AdvantHealth, which sells short-term plans underwritten by American Financial Security Life Insurance. Together they paid $490 per month. To enroll, she answered health eligibility questions, including if she was pregnant, undergoing fertility treatment or in the process of adopting a child.

The questionnaire also asked if in the past five years she or her husband had been diagnosed or treated for, or had taken medication for, about two dozen conditions, including cancer, stroke, heart disease and diabetes. It asked if they had mental health issues or alcohol or drug dependency, and if she or her husband were obese.

Black marked “no” to all. Endometriosis was not on the list. Yet one day at a physical therapy session, she was told the bills for her visits were not being paid. Black said the insurer told her it was probably a clerical error.

But then Black got a benefits explanation showing that her plan had indeed paid nothing. When she called again, she said, she was told all her claims had been denied because her endometriosis was not covered. “It never occurred to me to specify I had had endometriosis. I said I had just had surgery for it, and I was told I would be covered,” Black said, adding that she was dumbfounded that a preexisting condition could be denied. “I didn’t think they could do that anymore.”

Between premiums and uncovered care, Black faced more than $4,000 in out-of-pocket costs from the few months she had her policy. She caught a break when the employer-sponsored plan at her new job agreed to pay about half of the previous claims. She filed a complaint with the Texas Department of Insurance against the short-term insurance company and the broker who sold coverage to her, alleging deceptive marketing and failure to pay claims.

She lost. The state agency wrote to Black in July 2020 and said, “The claims were denied correctly due to non-covered services.”

The letter further said TDI could not intervene between Black and the broker and suggested she hire a lawyer.

AdvantHealth did not respond to email and phone requests for comment.

On March 11, President Joe Biden signed into law a massive $1.9 trillion economic package known as the American Rescue Plan. Tucked inside was an extension of the special enrollment period to sign up for ACA-compliant plans, subsidizing COBRA payments that could help people keep their existing health coverage after leaving or losing jobs, and expanding the federal assistance that lowers ACA plan premiums.

But will it be enough to transition people out of non-ACA-compliant plans?

Some health policy experts worry that many who have short-term and other noncompliant plans do not yet realize those plans’ limits and, even if they do, may be reluctant to switch.

Just having the option to change plans may be insufficient. “It will take the same level of intentionality that got people on these plans to get them off of them,” said Dorianne Mason, director of health equity for the National Women’s Law Center.

Smedsrud, the Pivot Health CEO, said he recently sent emails to his short-term plan members to tell them they might now be eligible for a subsidy that could help them afford a more comprehensive plan and should consider switching — even if it meant he lost customers.

He insisted short-term plans have a place but said they should never be sold as or considered a substitute for comprehensive coverage. He also acknowledged there were some industry “bad apples” who are taking advantage of the confusion.

“I would not be opposed to reforms in short-term plans,” he said, including reinstating limits on duration. “Shame on all of us if some people feel tricked.”

Did you receive high medical bills for COVID-19 testing, treatment or lasting complications that your insurance did not cover? We want to hear from you. Fill out the questionnaire below or email [email protected] to get in touch.

Are you a public health worker, medical provider, elected official, patient or other COVID-19 expert? We’re looking for information and sources. Help make sure our journalism is responsible and focused on the right issues.

May 12, 2021: This story originally misstated when short-term plans were limited to three months. It was an Obama administration rule change, not part of the Affordable Care Act.

Maya Miller contributed reporting.

Update, May 10, 2021: This story was updated to note that on Monday, a Mather spokesperson confirmed a check for $32,772 had been received and that the remaining balance would be waived by the hospital.