ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up to receive our biggest stories as soon as they’re published.

This article is co-published with The Texas Tribune, a nonprofit, nonpartisan local newsroom that informs and engages with Texans. Sign up for The Brief Weekly to get up to speed on their essential coverage of Texas issues.

As she waited for the results of her rapid COVID-19 test, Rachel de Cordova sat in her car and read through a stack of documents given to her by SignatureCare Emergency Center.

Without de Cordova leaving her car, the staff at the freestanding emergency room near her home in Houston had checked her blood pressure, pulse and temperature during the July 21 appointment. She had been suffering sinus stuffiness and a headache, so she handed them her insurance card to pay for the $175 rapid-response drive-thru test. Then they stuck a swab deep into her nasal cavity to obtain a specimen.

De Cordova is an attorney who specializes in civil litigation defense and maritime law. She cringes when she’s asked to sign away her rights and scrutinizes the fine print. The documents she had been given included disclosures required by recent laws in Texas that try to rein in the billing practices of stand-alone emergency centers like SignatureCare. One said that while the facility would submit its bill to insurance plans, it doesn’t have contractual relationships with them, meaning the care would be considered out-of-network. Patients are responsible for any charges not covered by their plan, it said, as well as any copayment, deductible or coinsurance.

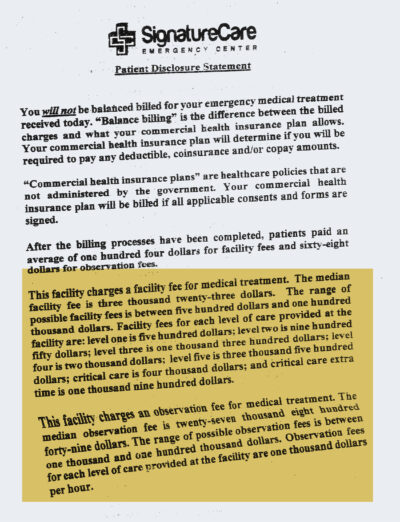

The more she read, the more annoyed de Cordova became. SignatureCare charges a “facility fee” for treatment, the document said, ranging “between five hundred dollars and one hundred thousand dollars.” Another charge, the “observation fee,” could range from $1,000 to $100,000.

De Cordova didn’t think her fees for the test could rise into the six figures. But SignatureCare was giving itself leeway to charge almost any amount to her insurance plan — and she could be on the hook. She knew she couldn’t sign the document. But that created a problem: She still needed to get her test results.

Even in a public health emergency, what could be considered the first rule of American health care is still in effect: There is no set price. Medical providers often inflate their charges and then give discounts to insurance plans that sign contracts with them. Out-of-network insurers and their members are often left to pay the full tab or whatever discount they can negotiate after the fact.

The CARES Act, passed by Congress in March, includes a provision that says insurers must pay for an out-of-network COVID-19 test at the price the testing facility lists on its website. But it sets no maximum for the cost of the tests. Insurance representatives told ProPublica that the charge for a COVID-19 test in Texas can range from less than $100 to thousands of dollars. Health plans are generally waiving out-of-pocket costs for all related COVID-19 treatment, insurance representatives said. Some costs may be passed on to the patient, depending on their coverage and the circumstances.

As she waited, de Cordova realized she didn’t want to play insurance roulette. She changed her mind and decided she’d pay the $175 out-of-pocket for her test. But when the SignatureCare nurse came to collect the paperwork, de Cordova said the nurse told her, “You can’t do that. It’s insurance fraud for you to pay for our services once we know you have insurance.”

Dr. Hashibul Hannan, an emergency room physician, lab director and manager at SignatureCare, told ProPublica his facility is an emergency room that offers testing, not a typical testing site. He said de Cordova should have been allowed to pay the $175 cash price. The staff members were concerned about being accused of fraud because they had already entered her insurance information into the record, he said. So they didn’t want it to appear she was being double-billed. Hannan also said he regrets that she was upset by the disclosure forms that are now required under state law.

Unable to pay cash and unwilling to take a chance on the unknown cost, de Cordova decided to leave without getting the results of her COVID-19 test.

“I Would Have Signed Anything”

Later that day, de Cordova couldn’t get past what happened. She wondered what happened to patients who didn’t read the fine print before signing the packet.

Then she realized she and her husband, Hayan Charara, could investigate it themselves. In June, the couple’s 8-year-old son had attended a baseball tryout. They thought the kids would be socially distanced and that precautions would be taken. But then the coaches had crowded the players in a dugout, with no masks or social distancing, and a couple days later the boy said he wasn’t feeling well.

So just to be safe, on June 12, Charara took their son to the same SignatureCare, the Heights location, for a COVID-19 test. The line was so long they had to wait for hours, go home, come back and wait for hours again in their car in the 100-degree heat. Charara, a poet who teaches at the University of Houston, said he didn’t take a close look at the financial disclosure paperwork. De Cordova wasn’t with them. It had been 10 hours of waiting by the time the boy was tested, so “I would have signed anything,” he said. (The child tested negative.)

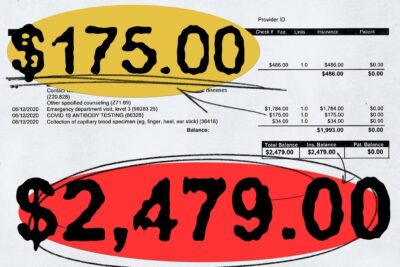

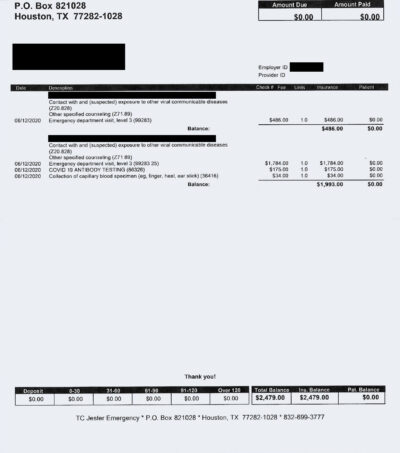

Charara, de Cordova and their children are covered by the Employees Retirement System of Texas, a taxpayer-funded benefit plan that covers about half a million people. They hadn’t received any notices about the charges for their son. So they contacted the SignatureCare billing department and asked for an itemized statement. The test charge was indeed $175. But the total balance, including the physician and facility fees associated with an emergency room visit, came to $2,479.

The facility fee was $1,784 and the physician fee $486.

The couple were dumbfounded. Their son’s vital signs had been checked but there had been no physical examination, they said. The interactions took less than five minutes total, and the child stayed in the car. “You’re getting a drive-thru test, and they’re pretending like they’re giving you emergency services,” de Cordova said.

The SignatureCare charges shocked experts who study health care costs. Charging $2,479 for a drive-thru COVID-19 test is a “nauseating” example of profiteering during a pandemic, said Niall Brennan, president and CEO of the Health Care Cost Institute, a nonprofit organization that studies health care prices. “It’s one of the most egregious examples of giving the fox the keys to the henhouse I’ve ever seen and yet another example of the absurdity of U.S. health care pricing.

“Imagine a vendor in any other walk of life being allowed to bill a third party for whatever amount they wanted,” Brennan said.

Insurance companies in Texas typically pay between $100 and $300 for drive-thru COVID-19 tests, said Jamie Dudensing, CEO of the Texas Association of Health Plans. But the association’s members have seen hundreds of out-of-network COVID-19 test charges come in far higher, some in the thousands of dollars.

“There’s no excuse for that, especially in a public health crisis,” said Chris Callahan, spokesperson for Blue Cross and Blue Shield of Texas, which likewise has seen high charges for COVID-19 tests from out-of-network providers.

The reimbursement rates negotiated between insurance companies and in-network providers are much lower, but they still vary, according to data provided by the nonprofit FAIR Health, which tracks spending by private insurers. For the same test billed by SignatureCare, an in-network insurer pays a median price of $23 in Utah and $75 in Wisconsin, according to FAIR Health estimates.

Texas is notorious for its high-priced out-of-network emergency bills and free-standing emergency departments. Some of the facilities appear to be using COVID-19 testing to draw in patients so their insurance plans can be charged for additional services, said Blake Hutson, associate state director for AARP Texas, the advocacy organization for older Americans. “It’s not a surprise they would be racking up the charges and adding on everything they can and billing the health plan,” he said.

In some cases, insurers do pay the exorbitant out-of-network charges, Hutson said, but they typically get reduced. In 2019, Texas lawmakers voted to ban billing patients in state-regulated insurance plans for charges not covered by their policy, Hutson said, which is known as “balance” or “surprise” billing. But consumers may still be responsible for any deductibles and other cost-sharing under their health plan. And the costs covered by the health plan get passed back to the consumers over time in the form of higher premiums, he said. “It’s all problematic for the cost of care,” Hutson said.

Hannan defended SignatureCare’s high out-of-network charges by blaming insurance companies for refusing to give what he considers to be fair in-network rates. The charges are a starting point for negotiating a fair deal from out-of-network insurance plans, he said. He described SignatureCare, which has 18 locations, as “small players. When it comes to negotiating with insurance companies, we have no luck.”

Was the Bill Accurate?

The medical record portrays the visit as an emergency and contains details that are not consistent with how Charara and de Cordova describe their son’s condition. The chief complaint in the record is “body fluid exposure,” and elsewhere it says “confirmed COVID exposure.”

But that’s not accurate, according to the parents. No one had coughed or sneezed on their son, and they knew of no one from the tryout who had tested positive for COVID-19, they said. The child’s temperature is registered in the record as 102.8, which is high. But Charara said that could have been caused by sitting in the Texas heat, waiting for the test.

Shelley Safian, a Florida health care coding expert who has written four books on medical billing, examined the bill and medical records of Charara and de Cordova’s son at ProPublica’s request. She said the medical records don’t justify the charges. SignatureCare billed the case as if the exam were an emergency that required an “expanded problem focused history” and “medical decision making of moderate complexity,” she said.

In order to qualify for reimbursement of an exam at that level, the encounter would need to include examining the affected organ system, Safian said. But the medical records do not document any check of the respiratory system, which would be indicated for suspected COVID-19.

Much of the medical record appeared to be cut and pasted from other electronic records, Safian said. “This is boilerplate B.S.,” she said, “and I don’t mean ‘bachelor of science.’”

Hannan, the SignatureCare doctor and manager, stands by the charges associated with the child’s COVID-19 test. The facility has to treat every case like a possible emergency, and that requires an examination, he said. He pointed out that the charges are in line with what other out-of-network providers would charge in the area, according to FAIR Health, though they are far higher than in-network prices.

A doctor’s examination may not be as hands-on during COVID-19, but, similar to a telemedicine visit, a lot can be examined visually, Hannan said. Hannan said the company he uses for coding said COVID-19 requires a higher level of care and vigilance because it’s an infectious disease.

In light of the questions raised by ProPublica and Safian, Hannan said he asked his billing company to audit the charges. Sharon Nicka, president and CEO of Nicka and Associates, the billing company used by SignatureCare, took issue with Safian’s assessment and said the billing codes used were justified by the medical record. She said the charges are high for a drive-thru test, but those are set by SignatureCare.

ProPublica identified several apparent errors and contradictions in the medical record and billing documentation. For example, the notes in the medical record alternatively refer to the boy as “symptomatic” and “asymptomatic.” The record also says the physical exam showed a skin wound that “was not red, swollen or tender,” but the child had no wound of any kind, the family said. And the billing documentation shows a charge for an antibody test when the medical record showed that the patient actually received a diagnostic test, which is something different.

In response to ProPublica’s questions, a SignatureCare medical director reviewed the record. The error about the “wound” may have been caused by a software template adding something that was not in the physician chart, the reviewer wrote. The facility now uses a different template. The charge for the antibody test is likely a billing error, as the physician had ordered the correct test, the reviewer wrote. “We will continue to update and improve our (electronic medical records),” the reviewer said.

Hannan stressed that SignatureCare is upfront with patients about the possible fees associated with its treatment, including the disclosure paperwork and explanations on its website. It’s an emergency room, he said, so patients should expect emergency room fees. Patients who do not have a medical emergency should not come, he said, though the ER allows patients to book appointments a day in advance for a COVID-19 test.

Dudensing, the chief executive of the Texas Association of Health Plans, said she’s heard Hannan’s contention before and it’s true that freestanding emergency rooms have a license that allows them to charge more. But she still believes that they handle many nonemergency cases and are forcing facility fees of thousands of dollars on them. “They’re hiding under the guise of emergency rooms when they’re really dressed-up urgent care,” she said.

Diana Kongevick, director of group benefits for the Employees Retirement System of Texas, said the health plan had only recently received the bill for the 8-year-old’s test. It hadn’t been processed, so she could not speak to it directly. But, in general, the health plan will pay 100% of the cost of the test, in this case $175, she said. The claim would be processed using out-of-network provisions, she said. So for the other charges, the patient may be responsible for paying in the range of $600, she estimated, for the out-of-network copay and deductibles. “This is a nonemergent patient self-referral to an out-of-network provider,” Kongevick said.

“Testing Should Be Free”

Even if the Employees Retirement System of Texas determines that Charara and de Cordova should pay $600 for their son’s test, SignatureCare will not be sending the family a bill, Hannan said. He said insured patients are not being sent bills for COVID-19 treatment beyond what their insurance companies cover.

De Cordova never did get her test results, and she didn’t seek a test elsewhere. She felt better later and now believes she had just been suffering from allergies. But what if it had turned out to be COVID-19, she wondered. Might she have gone on to infect others, she’s asked herself.

From a public health perspective, the haggling about out-of-network charges and payments puts patients in the middle, and it might discourage them from getting tested for COVID-19 during the pandemic, said Stuart Craig, an economist at the University of Pennsylvania who studies health care costs. “It’s another part of the fragmentation of the health care system that makes patients’ lives miserable,” Craig said.

It’s especially frustrating, he said, because COVID-19 testing is so essential to making it safely through the pandemic. Craig said he believes there should be a nationally mandated price and government subsidies to make sure medical providers and manufacturers are motivated financially to provide tests. “Testing should be free,” Craig said. “In fact, we should probably be paying patients to get tested.”

Do you have a story to share with ProPublica about billing practices related to COVID-19 testing or treatment? Please complete our form to tell us about it.

Filed under: