ProPublica is a nonprofit newsroom that investigates abuses of power. Sign up to receive our biggest stories as soon as they’re published.

This article is co-published with The Texas Tribune, a nonprofit, nonpartisan local newsroom that informs and engages with Texans. Sign up for The Brief Weekly to get up to speed on their essential coverage of Texas issues.

HOUSTON — On an afternoon in mid-June, Analleli Solis was walking home from her brother’s house just down the street when she noticed someone she didn’t know retreating from the front door of her modest brick home.

Solis approached the woman, who handed her an envelope.

Inside was a lawsuit from Oportun Inc., a personal loan company Solis had turned to for years when she and her husband didn’t have enough cash to cover rent, fix their cars or take a vacation.

Now, the company was suing Solis to recoup some of that money, demanding $4,196.23 including fees and interest.

Solis’ shock quickly gave way to anger. Three months earlier, after she missed a few of her $130 bimonthly payments, she said she called Oportun to tell the company she had lost her jobs as a hotel housekeeper and fast food worker because of the coronavirus pandemic and needed some relief.

The 43-year-old mother of three expected the company would understand.

She was a longtime customer, after all. Her latest loan, which she took out to repair her aging SUV, was her fifth with Oportun since 2013, she said, and she had never missed a payment. Staffers were always friendly and helpful.

Silicon Valley-based Oportun, a subprime installment lender that operates in 12 states, also portrayed itself as a financial ally to the Latino immigrant community, its primary customer base, and had built a reputation as a more affordable and humane alternative to payday lenders. In its business filings and on its website, the company — whose name is short for “oportunidad,” Spanish for opportunity — claimed to work with borrowers grappling with cash-flow problems beyond their control. Just two weeks into the pandemic, it announced a special hardship program that postponed payment due dates as long as impacted customers notified the company in advance.

But over a series of phone calls, Solis said, Oportun agents told her there was nothing they could do to help her, even though her financial situation was particularly dire as her husband had also recently lost his job. She said they didn’t offer a payment plan or mention the hardship program.

“I feel powerless not being able to pay them,” Solis, who immigrated from Mexico as a teenager, said in Spanish.

Solis is among tens of thousands of Oportun borrowers who have found themselves in a similar predicament in recent years, according to a monthslong investigation by ProPublica and The Texas Tribune that drew on more than a million Texas court records, hundreds of pages of company financial filings, and interviews with more than a dozen consumer advocates, attorneys and industry experts.

Our reporting revealed a company that draws clients in by depicting itself as a benefactor of the Latino immigrant community yet charges high interest rates, keeps customers like Solis on the hook with repeated refinancing and routinely uses lawsuits to intimidate delinquent borrowers into paying again.

An analysis of court records in nine of Texas’ largest counties — home to the vast majority of the 80 kiosks and strip mall storefronts the company operates in the state — found that Oportun has sued borrowers after they fell behind on their payments more than 47,000 times from May 2016 through July of this year. That’s 30 lawsuits per day on average.

So far this year, Oportun has filed nearly 10,000 lawsuits against customers in those counties, with more than half of those coming after the World Health Organization declared the coronavirus a pandemic in mid-March.

That number of filings makes Oportun the most litigious personal loan company in Texas and one of the most litigious debt collectors in the state overall this year. It is rivaled only by larger companies like Conn’s HomePlus, Capital One and a handful of firms that buy unrecovered debts from banks and other creditors.

Asked why it sues so many of its customers, particularly during a pandemic, Oportun referred ProPublica and the Tribune to a recent blog post from company CEO Raul Vazquez that said the company used lawsuits as “a mechanism of last resort to get the small minority of our customers who have fallen behind in their payments and not answered our calls, letters, texts or emails for several months to reengage with us.”

That was the case with Solis, according to a statement Oportun released after she gave the company permission to comment on her account.

“According to our records, this customer did not reach out to us and was unresponsive to our repeated attempts to reach them,” the statement said, adding that “if a customer tells us they are impacted by the pandemic, they are eligible for our emergency hardship programs.”

Vazquez defined the “small minority” of loans resulting in lawsuits as less than 6% over the past five years. Though he didn’t say how many lawsuits that represented, he said that it had “become a big number” over time and announced that the company would drop all pending debt claims — including the one against Solis — and temporarily suspend the filing of new ones. He also vowed to reduce the company’s filing rate by more than 60% and cap interest rates at 36%, an annual percentage rate that consumer advocates consider an absolute maximum for smaller personal loans. (While the company says its average APR is already 36%, ProPublica and the Tribune found that it has often charged rates as high as 66.99% in Texas and California.)

The blog post came after the company discovered that reporters from ProPublica and the Tribune, as well as The Guardian, were investigating its debt collection practices in Texas and California.

“We have always designed our products and practices to benefit our customers, so we asked ourselves how we can better serve our customers, especially in the current environment, while keeping our commitments to other stakeholders,” wrote Vazquez, a former Walmart executive who grew up in El Paso. “After extensive discussions and with enthusiastic support from our leadership team and Board, we have decided that we can do better and I’m writing today to share how we intend to do that on a permanent basis.”

Vazquez acknowledged that his company had become the No. 1 filer in small claims courts in both states. Still, the ProPublica/Tribune analysis shows Oportun has filed so many lawsuits that it would remain among the most litigious debt collectors in Texas even if it filed 60% fewer debt claims.

The company declined to make Vazquez available for an interview or respond to an exhaustive list of written questions regarding its legal collections strategy and general business practices.

Instead, it released a one-paragraph statement that touted its high customer satisfaction scores and rates of repayment. It also said it had enrolled more than 112,000 customers in its emergency hardship deferral program since the start of the pandemic, representing a total loan balance of more than $300 million.

“[Oportun is] consistently recognized by leading consumer advocates as a company that does right by its customers,” the statement said. “We are proud to have proven that it is possible to lend responsibly in low-and-moderate income communities and we are proud to receive customer satisfaction scores that are consistently on par with beloved brands like Ritz-Carlton, Apple, and USAA.”

But the same consumer advocates and legal aid groups who have recognized Oportun as a bright spot in the largely predatory world of subprime lending said they were disturbed by the scope of its legal collections activity. While the share of the company’s loans that lead to lawsuits may seem low, they said the rate is far higher than that of its peers — particularly for a lender that paints itself as a flexible benefactor. The ProPublica/Tribune analysis of the company’s loan originations show that its 6% filing rate would translate to well over 100,000 lawsuits.

Consumer advocates and legal aid groups also noted that the company has been certified for years as a Community Development Financial Institution, an esteemed federal designation for banks, credit unions and other lenders with clienteles that are largely low-income or in underserved communities of color, and said its collections practices fly in the face of that title.

Ann Baddour, director of the Fair Financial Services Project at the nonprofit advocacy group Texas Appleseed, said the scope of Oportun’s legal collections activity is “really problematic.”

“We’ve generally seen them as a positive player in the marketplace, so it was really shocking to me to see them as a major filer,” Baddour said, when informed of the publications’ findings. “We hope they will revisit their collections practices and look at aligning them with the community development mission that they have long highlighted as key to their business model.”

Baddour is particularly familiar with Oportun as she recently served alongside Vazquez on the Consumer Advisory Board of the Consumer Financial Protection Bureau, the federal watchdog agency formed in the wake of the 2008 financial crisis to better guard Americans from abusive lending practices.

Other consumer advocates say the measures Vazquez announced don’t address what they see as the root cause of the problem: Oportun lends money to people who can’t pay it back and not just during the pandemic. That’s evident not just from its voluminous lawsuits, but also its practice of refinancing high-interest loans, which makes it appear that borrowers have paid them off but actually keeps them on the hook, sometimes for years.

“When we saw the announcement, we didn’t immediately pop any Champagne bottles,” said Kiran Sidhu, policy counsel for the Center for Responsible Lending’s state policy team. (The center was started with support from the Sandler Foundation, which provided most of the original funding for ProPublica and remains its largest donor.)

Oportun’s Origin Story

Oportun — originally called Progreso Financiero — was founded in 2005 by James Gutierrez, the grandson of Mexican immigrants, who launched the company while earning his master’s in business administration at Stanford Business School. His vision was to help Latino immigrants gain access to mainstream financial services — and prove that subprime lending with zero collateral could be done compassionately and profitably with the right kind of underwriting.

“I wanted to make a big impact on our social problems in America, and I wanted to do something that helped the Hispanic community find economic opportunities,” Gutierrez told Bloomberg TV in 2009, the year he turned 32.

While his grad school friends joined Wall Street hedge funds, Gutierrez set up folding card tables at Latino supermarkets in California and spent half a year trying to prove to angel investors that he could successfully lend to people with modest incomes and negligible credit histories using a scoring system that took into account hundreds of unique attributes to determine the likelihood an applicant would repay a loan.

He never broke even, but succeeded enough.

Before he left the company in early 2012, Gutierrez — who founded a competing firm a year later — had closed tens of millions of dollars in new funding from major players including Madrone Capital, run by the eldest son of Walmart founder Sam Walton, and Greylock, known for its early investments in tech startups like Facebook. The infusions bankrolled the opening of dozens of kiosks and storefronts in California and Texas, the states with the largest Latino populations.

The week after his departure from the company, Gutierrez told the Los Angeles Times that Progreso was finally on track to break even. But that wouldn’t happen for years, even after Vazquez took the helm.

Under Vazquez, the company has expanded into 10 more states, started offering auto loans and an Oportun-branded credit card, and executed a major rebranding and overhaul of its marketing and public relations strategies. Last September, the company went public.

To date, it’s disbursed more than 3.9 million loans totaling more than $9 billion. At the end of 2019, it had nearly 800,000 active customers, its first annual filing shows.

Revenues are up in recent years thanks to the expansion, and the company has reported five consecutive years of pre-tax profitability. But business filings show that as its operating expenses have soared, its profits have been modest and spotty.

In the first two quarters of 2020, Oportun’s net profits dropped by $50 million, compared with the same period in 2019, amid the widespread economic fallout from the COVID-19 pandemic.

In its 2019 year-end filing to the U.S. Securities and Exchange Commission, Oportun explained the financial challenges ahead, saying it would need to continue with its rapid expansion to “achieve and increase profitability.”

Even if it succeeded, it said “we may not be able to maintain or increase our level of profitability over the long term.”

Oportun’s Business Model

Nearly a decade ago, Texas Appleseed — Baddour’s group — highlighted Oportun in a report as one of several new, non-bank players striving to offer affordable small-dollar loans. But, it said, few had reached significant scale.

Many statistics would indicate Oportun is bucking the trend. It added hundreds of retail locations across the country in the past five years and has grown its active customer count by more than 300,000 since 2016. In a filing announcing its initial public offering, it said that the vast majority of dollars lent had been repaid.

“Our track record as a responsible lender is clear — 92% of our customers have historically paid us back on time and in full,” Oportun said in a statement to ProPublica and the Tribune, adding that its so-called loss rates compare favorably to prime lenders.

But consumer advocates say the large number of lawsuits Oportun is filing raises the question: Under what circumstances are those repayments occurring?

The company wouldn’t say how much money it has recouped after “reengaging” customers via the legal system. And the ProPublica/Tribune investigation found that the company has other ways to retain borrowers that consumer advocates describe as questionable.

Under its “Good Customer Program,” Oportun allows borrowers to take out larger loans with lower interest rates, which typically translates to lower monthly payments. To qualify, they must have never missed a payment, maintained their current loan for a year or paid off 40% of it.

“If a customer stays with us, we give them more capital and drop their rate,” Vazquez, the Oportun CEO, said last month in an interview with the nonprofit Financial Health Network, in which he described the average Oportun borrower as 42 years old with a family to support and a $45,000 annual salary. “A customer should see a benefit for performing well on their loan.”

But consumer advocates and attorneys say the program can trap consumers in a cycle of debt because they are repeatedly rewriting potentially unaffordable loans, thus paying more interest than principal.

“In general, a model that pushes refinancing is not a good idea,” said Lauren Saunders, associate director of the National Consumer Law Center. “Refinancing is masking troubles.”

Oportun doesn’t disclose its refinancing rate or how many customers are enrolled in its “Good Customer Program,” but figures in its public filings and other publicly available information show the company depends heavily on repeat customers, which have comprised some 80% of its principal balance since at least 2017, according to the company’s latest annual filing. And the 3.8 million loans the company has disbursed to date have gone to about 1.7 million people, meaning each person takes out an average of more than two.

A significant share of the company’s revenue — more than 90% — comes from interest income, though that includes late fees.

Solis, the hotel worker in Houston, said she took advantage of refinancing several times. She doesn’t recall whether her payments or interest rate dropped as a result but said she found the $130 bimonthly payments on her most recent $6,000 loan reasonable.

In its statement regarding Solis, Oportun said, “Each loan came after the customer had paid down a substantial portion of their balance, each loan came with a lower APR, and the customer’s credit score was steadily improving.”

Solis said her daughter tried to borrow from Oportun to help cover payments, but she was denied.

“It’s really hard to get sued for something that’s out of your control,” she said.

Despite Oportun decreasing its interest rates with each refinance — compared with payday lenders that peddle short-term, single-payment loans with APRs that can top 400% — they are still high.

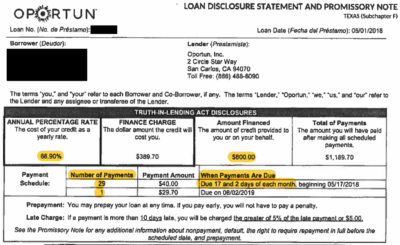

In May 2018, Oportun lent $800 at a 66.9% interest rate to a woman in McAllen, a city on the Texas-Mexico border, who needed it to pay rent. The terms: 15 months with bimonthly payments of $40. (That meant she would have paid a total of $1,189.70, including $389.70 in interest.)

But even that was too much. Struggling to juggle other loans, the woman defaulted, and Oportun sued her last year.

Her pro bono attorney, Amy Clark of Texas RioGrande Legal Aid, was able to settle the case by arguing that Oportun had harassed her client during the collections process by repeatedly calling the personal references the woman gave when she applied for the loan.

“They had collected information on ‘references’ as though it was to get the loan, but it was for collection purposes,” she said.

Despite the near 67% interest rate in her client’s loan, Oportun maintains that its average APR is 36%. But it doesn’t disclose comprehensive data on its rates or fee structure and declined to disclose its median interest rate, a better indicator of the rate it typically charges.

Some websites that review credit products for consumers have pointed to that lack of transparency as a red flag and advised consumers to seek other options before borrowing from Oportun.

“Oportun loans are expensive, though the company is not transparent about their overall rates and fees, which vary by state,” according to a May review in WalletHub, which noted that Oportun’s opaqueness brought its score down considerably despite the company’s “positive reputation.”

The Texas Office of Consumer Credit Commissioner, the state agency that regulates lenders, declined an open records request for Oportun’s lending disclosures, which shed light on the number of loans disbursed and interest earned, citing confidentiality. But similar reports from California’s Department of Business Oversight show that last year Oportun charged APRs between 40% and 69.99% on nine out of every 10 loans under $2,500 issued or refinanced in that state.

With those kinds of interest rates, the main reason Oportun’s loans are more affordable is that the company allows customers to pay them back in installments with terms that range from six to 48 months. But Baddour of Texas Appleseed said multiyear terms for these kinds of consumer loans can become burdensome for borrowers who struggle to maintain consistent income.

The Lawsuits

In 2010, Oportun obtained its first batch of operating licenses in Texas and now has 80 grocery store kiosks and strip mall storefronts in more than a dozen counties across the state.

Court records covering nine of the state’s most populous counties show that Oportun didn’t start suing borrowers until 2016, when its expansion was well underway, the ProPublica/Tribune analysis found.

That year, Oportun filed at least 3,500 debt claims in three of the largest Texas counties, those home to Houston, Dallas and Fort Worth. Its filings have grown every year since then.

Oportun sued more than 9,000 borrowers during the first half of 2020, nearly 2,500 more than it did in the same period of 2019, the analysis found. In Harris and Dallas counties, where more detailed records are available, the median claim amount this year is about $1,400.

Consumer advocates and attorneys say Texas’ court system also makes it efficient for Oportun to sue.

Records show that non-attorney staffers called “legal collections specialists” — some of them straight out of college — file lawsuits en masse in justice of the peace courts, where claims are capped at $10,000, you don’t have to be an attorney to sue and filing fees, typically about $50, are hundreds of dollars less per case than in county or state courts.

“I think it just doesn’t cost them that much, so why not?” said Anderson Simmons, an Austin-based consumer attorney who regularly represents consumers in debt collection cases, though never against Oportun. “They have to pay employees to fill out the forms, but they could have someone doing that for $15 an hour, so it’s probably just a mass assembly line.”

In his July blog post, Vazquez described Oportun’s legal collections activity as a success. That’s why the company has dropped some two-thirds of the lawsuits it’s filed, he explained.

Mary Spector, who directs the civil and consumer law clinic at Southern Methodist University’s Dedman School of Law, said that suing a debtor with no intention of litigating the case is an abuse of the legal system.

“It smells like harassment and intimidation,” she said. “Especially when cases are filed in large numbers.”

Carl Smart, a Dallas-based consumer attorney who regularly represents borrowers in Oportun suits, said Oportun staffers always move to dismiss cases as soon as they realize the borrower has an attorney.

Smart said that’s unusual because “these kinds of cases are generally fairly easy for the creditor to win because all they have to do is prove the debt is this person’s.”

Like Solis and other borrowers ProPublica and the Tribune interviewed for this story, Smart said it is often hard to get through to Oportun by phone.

Smart said many of his clients are Latino immigrants who don’t speak English or understand the difference between a civil and criminal lawsuit.

“They don’t understand their rights. They think they’re going to jail,” Smart said. “I do kind of think that Oportun takes a little bit of advantage of that.”

Oportun’s contracts say borrowers are considered in default if they miss just one payment and must immediately pay the full amount remaining on the note — and that the company doesn’t have to notify them in advance that it will demand they do so.

Borrowers have very little recourse unless they specifically opt out of provisions in the contract that bar them from joining a class action lawsuit against the company or taking disputes to trial, but legal aid and private consumer attorneys said that rarely happens.

Most of those provisions are standard in consumer contracts. But they “are what allows these companies to operate at will, because individual cases are like bug bites to them,” said Clark of Texas RioGrande Legal Aid.

Consumer advocates and attorneys say Oportun’s legal strategy is also likely effective because many of its borrowers are undocumented and fear the legal system.

Oportun allows borrowers to use an individual tax identification number in lieu of a Social Security number when they apply for loans, making them easily accessible to undocumented immigrants. Even then, others may use Social Security numbers that they borrow or buy when they arrive in the country.

Oportun declined to say how many of its borrowers might be undocumented, but a review of available petitions in the 467 lawsuits Oportun filed in June in Harris County shows the company had Social Security numbers on file for fewer than half of the defendants.

While Oportun drops two-thirds of the lawsuits it files, Baddour noted that it files so many in Harris County — where it has the most retail locations — that it also secures more rulings there than most other debt collectors. The vast majority of those are won by default because the defendant doesn’t respond to the lawsuit.

Very few Oportun defendants obtain lawyers, the ProPublica/Tribune analysis showed. Last year in Harris County, 105 out of 7,600 of them did, and it made a difference: Their cases were dropped 96% of the time before a ruling.

Like Solis, several Oportun borrowers said the lawsuits against them came as a surprise.

In late November, Augustine Ayala said he borrowed $300 to fix his car, but he fell behind on his payments totaling $30 a month after he contracted COVID-19 and was sent home from his warehouse job.

The 22-year-old, whose take-home pay was about $400 per week, was served at home on June 11 while awaiting a second negative diagnostic test so he could return to work. The lawsuit said he owed $305.28.

Ayala told ProPublica/The Texas Tribune in July that he was trying to pay the loan back, but it was challenging with interest still accruing.

“It just keeps going up and up and up, and I’m like … can y’all work with me?” he said. “It’s been stressful because I have to worry about still having to help my dad, I have to give him rent money every month, and then I still have to pay off this loan … and I don’t get that much of a check, you know.”

Oportun declined to comment on Ayala’s account without his written consent, which he didn’t provide prior to publication.

“You Don’t Get in Debt Because You Want To”

While Oportun has dropped all pending lawsuits and says it won’t file new ones for a while, it will remain one of the top debt collectors in the state under the measures it announced in late July. The ProPublica/Tribune analysis showed that even if Oportun reduced its legal filings by 60%, its ranking would only drop from second to fifth by year’s end.

Vazquez also didn’t specify how the 36% rate cap would be applied, including whether the company would charge that much on all its loans, which range from $300 to $10,000. Consumer advocates have long considered that APR an acceptable maximum for personal loans but only for smaller ones, limited to a few thousand dollars at most.

Thirty-six percent is also still far higher than interest rates on subprime credit cards, which hover around 25%.

Sidhu of the Center for Responsible Lending said none of the measures address what she points to as the root cause: Oportun is lending money to a lot of people who can’t repay, and its proprietary scoring model to determine whether an applicant will do so isn’t all that accurate.

“If they aren’t radically reshifting the way they understand their clientele, I don’t see any real impetus for meaningful change,” she said.

To Carla Nuñez, a Venezuelan immigrant and single mother who lives in suburban Houston, the Hispanic community is “easy prey” for Oportun.

She said Oportun approved her for a $6,000 loan last year even though she needed less than half that to cover a three-month deposit on a new apartment.

In a complaint filed with the state of Texas last year, Nuñez claimed that Oportun refused to arrange a payment plan with her when she fell behind on her $120 bimonthly payments after her teenage daughter was hospitalized with a rare breathing disorder and she had to quit one of her jobs to help care for her.

Nuñez is among at least three dozen people who have filed complaints against Oportun with the Texas Office of Consumer Credit Commissioner and Consumer Financial Protection Bureau since 2011. Complaints range from refusal to offer a payment plan to harassing phone calls to a legal threat.

Nuñez and Oportun resolved the matter without going to court, records show. She said she paid off her loan earlier this year after she got her income tax return. Still, she said, the ordeal had profound and long-lasting financial implications.

In a second complaint filed last December, Nuñez said that her credit score had been damaged after Oportun charged off her account, meaning it didn’t expect to be repaid, despite the fact that she had resumed payments. Because of that, Nuñez said she was unable to purchase a special breathing machine that her daughter needed.

“You don’t get in debt because you want to,” she said in an interview. “Their best weapon is hurting your credit, because they know that closes a lot of doors.”

Oportun declined to comment on Nuñez’s account without her written consent, which she did not provide prior to publication. But in its one-paragraph statement, it suggested the number of complaints Texans have lodged against it is small in comparison to the more than 800,000 loans it has disbursed in the state since 2014.

“Each of those complaints was investigated and cleared with no finding of any impropriety,” the statement said.

In Houston, Solis has been back at work for about two months now, but she’s also the sole provider for her household — her husband hasn’t been able to find another job — and is still struggling to catch up on bills after being unemployed for so long.

She received an email from Oportun on Aug. 5 saying it was dropping the lawsuit against her. She said it gave her some relief but that she is still uneasy knowing she can’t pay back what she owes.

“They have no compassion for what you’re going through,” Solis said. “They only care about the money.”

Chris Essig, Paul Kiel and Lexi Churchill contributed reporting.

Disclosure: Facebook, Southern Methodist University, Texas Appleseed and Walmart have been financial supporters of The Texas Tribune, a nonprofit, nonpartisan news organization that is funded in part by donations from members, foundations and corporate sponsors. Financial supporters play no role in the Tribune’s journalism. Find a complete list of them here.